Protection First. Your Family Comes Second to Nothing.

Most families are one paycheck away from financial collapse if something happens to a parent. Judeth Beverly helps middle-income families protect their income, structure their savings, and retire confidently.

Book Your Family Protection Review →

If Something Happened to You Tomorrow, Would Your Family Be Protected?

Most middle-income families are under-insured, under-saved, and over-dependent on a single income stream. One unexpected loss can collapse everything a family spent years building. That does not have to be your story.

Income

Disappears

Retirement Never Arrives

The Family Inherits Debt

This Is Not Insurance. This Is a Family Protection Plan.

Family Income Protection

Protection + Investment Strategy

Family Protection Review

Have Questions About Protecting Your Family?

Many families are unsure whether their current coverage is enough or how to structure protection the right way.

Share a few details and Judeth will personally reach out to help you explore the right path forward.

Testimonials

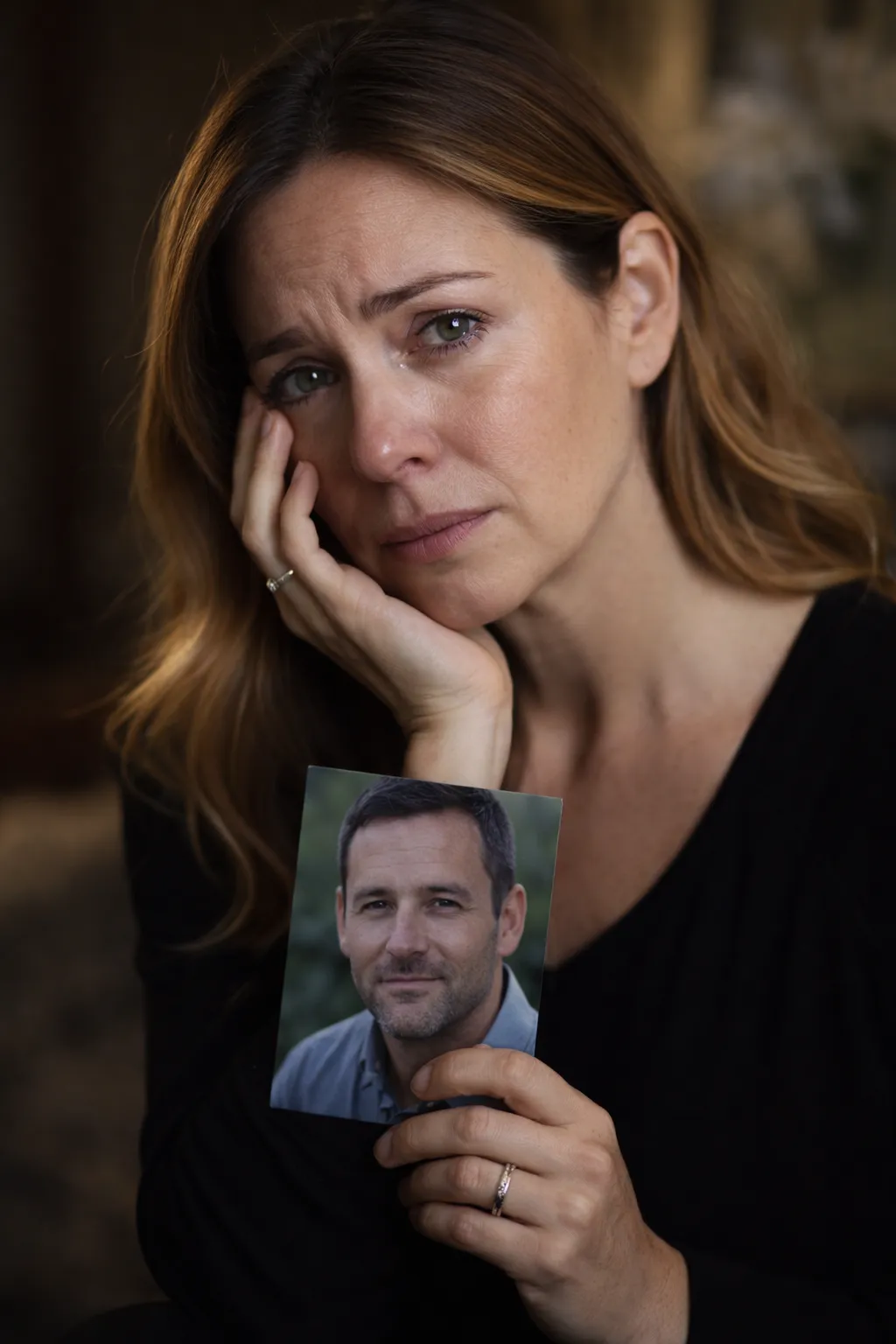

Maria Johnson

"I never thought I’d have to use life insurance this soon."

"When my husband passed unexpectedly, I was overwhelmed—not just emotionally, but financially. We had two young kids and bills that didn’t stop. Thankfully, we had life insurance in place. It covered our mortgage, daily expenses, and gave me time to grieve without the pressure of rushing back to work. That policy became our income when we needed it most. It truly protected our family when everything else felt uncertain."

Angel Reese

"Life insurance gave my family stability when I couldn’t."

"As the main provider, I always worried about what would happen if something happened to me. After being diagnosed with a serious illness, that fear became real. Because I had life insurance, I knew my children would still be financially secure—school, home, everything. It’s not just a policy—it’s peace of mind knowing your income is protected even when you’re not there."

David Allen

"It wasn’t about me—it was about them."

"I got life insurance because I didn’t want my family struggling if I wasn’t around. A close friend passed away without coverage, and I saw firsthand how hard it was on his family. That changed everything for me. Now I know that if anything happens, my wife and kids will still have income coming in. It’s one of the most important decisions I’ve made as a husband and father."

Frequently Asked Questions

Common Questions Answered for your convenience.

Do I realy need life insurance?

Yes—especially if anyone depends on your income or support. Life insurance helps replace lost income, cover funeral costs, pay off debts, and keep your family financially stable if something happens to you. Even stay-at-home parents provide valuable support that would be costly to replace..

Isn’t life insurance too expensive?

No—this is one of the biggest misconceptions. Many policies, especially term life insurance, are very affordable. In many cases, coverage can cost less than a daily coffee. The cost depends on your age, health, and coverage amount—but there are options for almost every budget.

What happens if I don’t have life insurance?

Without coverage, your family may be left to handle funeral expenses, debts, and everyday living costs on their own. This can create financial stress during an already emotional time. Life insurance provides a safety net so your loved ones aren’t burdened.

When is the right time to get life insurance?

The best time is now—before you actually need it. The younger and healthier you are, the lower your premiums will be. Waiting can lead to higher costs or even disqualification due to health changes..

What type of life insurance should I get?

It depends on your goals and budget. Many people get term life insurance because it's the most affordable, and provides more coverage for you and your family.

How much life insurance do I actually need?

A good rule of thumb is 10–15 times your annual income, but it really depends on your situation. You should consider your debts, mortgage or rent, children’s education, and daily living expenses. The goal is to make sure your family can maintain their lifestyle and stay financially secure if you’re no longer there.